Stormy weather

Most of all so by accounting standards

We’ve been having some brutal weather here at the ranch. The wind was blowing seventy miles per hour and the skies were ominously dark, even at noon. As long is it was only wind, I’d still go for a walk and at times, just let the wind blow around me from behind. But when the hail arrived, I rushed my way into the stable. Golf ball sized pellets of ice on my back, no thanks!

Two days later, the skies cleared up and now everything is back to normal. At least here at the ranch. Not so at Five Mile Ranch, though. Their equipment barn blew away and their tractors got pummeled by the hail. The tractors’ hoods look like a moonscape. Five Mile’s owner pulled up next to the pasture. He was weeping. “I took out a loan a few years ago for that barn and those tractors,” he said stammeringly, “it wasn’t even twenty percent paid off. I thought I’d get the money back from our insurance, but they refuse to pay, because they say we had ‘misquantified our climate risk.’”

My reaction was “climate risk?” What is that? This area is notorious for having violent storms. It’s part of the way of life around here, if your barn blows away, you have to rebuild it. Yes, the weather had been awful… but how was that related to “climate risk?”

According to some, a changing climate will lead to an increased intensity and frequency of extreme weather events. The insurance industry gladly adopted that belief in the early 2010s, since it would allow them to increase premiums in certain areas and for industries deemed to be at higher risk of “climate related events.” Therefore, financial actors such as lenders and insurance brokers started to collect information on corporate customers with the intent to quantify how much exposure they had to potential climate related damages. However, as they lacked a common set of standards, the results were hard to compare across the industry. That is where the group of the world’s twenty largest economies jumped in.

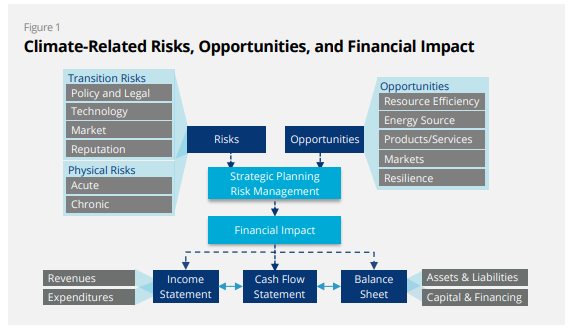

Back in 2017, the G20 nations organized a Task Force on Climate-Related Financial Disclosures (TCFD), which produced a report that outlined “standards for future financial reporting.” The task force started off from the assumption that “continued emission of greenhouse gases will cause further warming of the Earth and that warming above 2° Celsius (2°C), relative to the pre-industrial period, could lead to catastrophic economic and social consequences.” The task force had a broad look at societal impacts from climate change and the risk that those could pose to businesses. They categorized risk into “transition risks” and “physical risks” and put forth guidelines on how to assess those.

In the report, transition risks are further subdivided into four classes: “Policy and legal,” “Technology,” “Market”, and “Reputation.” While it may sound as prudent investor behaviour to try and quantify these risks, much of what the TCFD report lists as “transition risks,” appears to be a self-fulfilling prophecy. For instance, one bullet that resorts under “policy and legal” mentions “increased insurance premiums” as a risk to quantify. In other words: the “climate” risk of an increase in insurance premium needs to be quantified, such that business insurance premiums can be estimated more accurately, in a way that they account for the risk of increased premiums. Likewise, the “Market” and “Reputation” subsets list risks resulting from “shifts in customer preferences” and reputational damage from “stigmatization of sector [sic],” as well as from “reduced capital availability.” While the document does not say so directly, we can read the following between the lines: “We (the G20) plan to transition economies away from where they were back in 2010 by stigmatizing entire sectors (e.g. oil and gas), and by using the full force of government power and mainstream media propaganda to shift customer preferences away from those sectors. Businesses that fail to go along, will be classified as having ‘high climate risk.’ They will then have reduced access to capital, will be exposed to legal battles, and will be uninsurable.”

When it comes down to “physical risks,” the number of risks listed is more straightforward. At first, “acute” physical risks need to be quantified. These are detailed as “Increased severity of extreme weather events such as cyclones and floods.” Secondly, “chronic” physical risks need to be assessed as well, which are composed of risks owing to “changes in precipitation patterns and extreme variability in weather patterns,” to “rising mean temperatures” and to “rising sea levels.”

At this point, a good question to ask is how these risks can be assessed. A logical way to proceed would be to look at historical data and use those as a numerical basis to quantify the change. Let’s take the “severity of extreme weather events” as an example. For properties located somewhere near an ocean shore, that risk should be proportional to the increase in intensity of the storms recorded in recent times compared to a longer period of time. A plausible way to proceed to quantify the climate risk, would be to estimate the difference between the last fifteen years of hurricane intensity and hurricane intensity from a baseline period, e.g. 1970-2000. So, let’s have a look at the data. Climate Atlas is a frequently updated, US-based organization that tracks frequency and severity of storms, following the methodology from a 2011 peer-reviewed paper.

Figure 2 shows hurricane frequency as recorded from 1970 through the end of 2023. I could start performing statistical hypothesis tests here. I’m a many-trick pony. However, as a pony I have intuition and I know to trust my eyes. Do you see a major difference between recent years and the past century? If not, trust me, you don’t need a statistical test to tell you that there is no significant difference. It’s just like telling a mare from a stallion. You can do that without having pronouns specified.

If there is no increased frequency of storms, maybe they are getting more intense? Figure 3 plots the annual accumulated cyclone energy (ACE) over the same period. Different story?

There is no observable trend in either Figure 2 or 3. That is a fact that we can deduce from just reading the graph. However, recently, Italian scientists ran a statistical significance test on these data (through 2022) to confirm that there is no evidence that either hurricane frequency or intensity are increasing. That was one of their findings, which they published in a peer-reviewed paper. The findings in the Alimonti et al. paper were well aligned with expert knowledge from those “in the know” in the climate sciences and in some sense, just reiterating conclusions already reported in the report from the Intergovernmental Panel on Climate Change (IPCC).

Alas, their findings were not aligned with the acceptable opinion in the mainstream media. Both The Guardian and Agence France Presse (AFP) published smear articles claiming that “scientists” had “urged to retract” the paper. Let us at first acknowledge that this is not how scientific discussion typically proceeds. A paper can be retracted if its findings grossly misrepresent the data, if there is evidence of scientific fraud or if there is an obvious conflict of interest. In this case, none of those apply, as the paper’s findings largely align with the IPCC’s. So if this paper had focused on a subject other than climate change, its findings would have become the basis for a scientific discussion, which could be organized by letting other authors write papers critical of the original one and then asking the authors of the original one to write a rejoinder, all of which could be peer-reviewed as well.

None of that took place in this case. The paper was retracted by Springer Nature about a year after its original publication, merely based on journalists who interviewed a few scientists they had picked themselves, who were aligned with their own opinions. Notably, one of the scientists interviewed by The Guardian was none other than Michael Mann, who criticized the authors for being “another example of scientists from totally unrelated fields coming in and naively applying inappropriate methods to data they don’t understand. Either the consensus of the world’s climate experts that climate change is causing a very clear increase in many types of weather extremes is wrong, or a couple of nuclear physics dudes in Italy are wrong.” Note the lack of science or facts in this under-the-belt attack. Also, Mann thinks to be in a position to discern appropriate models from inappropriate ones, but allow us to remark here that Mann himself has demonstrated several times not to be too proficient at statistics, as for instance attested in the 2006 Ad Hoc Committee Report on the 'Hockey Stick' Global Climate Reconstruction, presented in the US Congress. Right now, Mann is predicting an “exceptional hurricane season” consisting of a “record-breaking 33 tropical storms” in the Atlantic. So far, we’ve been in for a total of three hurricanes and two tropical storms. Time will only tell if his forecast was right this time around.

The retraction of the Alimonti et al. paper is not only sordid from the perspective of the scientific community. It is also inconsistent with the mainstream media messaging to the broader public. Since the beginning of the COVID pandemic, we heard numerous mainstream voices urge not to cite any “unverified opinions,” even from experts. When a new pre-print was published that was not in line with the latest propaganda, media repeatedly rejected such studies for “not having passed peer review.” In the case of Alimonti et al., we have the opposite: a paper written by actual scientists has passed both editorial and peer review, only to be taken down by journalists, whose interviews do not contain any factual, scientific underpinning and therefore would never pass peer review. Also, the authors of the original paper have no way to respond to the smears in the press.

What happened to the Alimonti et al. paper, does of course not alter the underlying data. Those are quite clear: there is no discernible increase in either frequency or intensity of tropical storms. If there is no increase, why would we have to account for risk differently than we did a two decades ago? The risk seems to be the same … The answer is: because the G20 wants to steer the economy away from investments in certain sectors or geographies it does not like and wants to make the motivation for that look objective.

(If you like my objectivity, consider to subscribe!)

Another question to be answered here is: if there is no way to estimate the increase of storm frequency or intensity, then how should an accountant report them in a way that is compliant with the TCFD? The answer to that question is: by applying global climate models. Such global climate models can predict an increase in extreme weather events and allow for scenario evaluation. But the piece left out is that none of them manage to accurately predict the climate in the present. A recent analysis showed that the average of thirty-six widely accepted climate models overestimates present temperature increases by 43%.

In spite of their inaccuracy, global climate models are used as a cornerstone to estimate so-called “climate risk.” Of course, it requires a certain set of skills and familiarity with the models to apply them and then distill the forecasts down to a more granular, local level. Therefore, it should not surprise that an entire industry has mushroomed from the fertile soil of climate funding, that provides climate analytics and risk assessments. The global market for climate risk is estimated to measure $4 billion by 2027 and cannot be expected to disappear, since several countries, such as Britain and Brazil, have signed the TCFD report’s standards into law.

The climate risk industry is yet another example of a new sector that adds nothing to the material economy. Not unlike DEI, it has created an entire cadre of bureaucrats. Companies that do add value to the material world, could do entirely without their services. Should it come as a surprise that there is an increasing number of people who will label their own jobs as pointless? Doesn’t matter, corporate DEI bureaucrats will say. In their eyes, what matters is not employees excel at their jobs, but that they excel at creatively changing their pronouns on a weekly basis and that they repeat how much they support the Palestinian cause to free eastern Ukraine by just stopping oil and cow farts. The latter is obviously accomplished by pouring soup over paintings. That saves the planet, as long as it is soup from a vegetable broth that contains Impossible meatballs, so that it does not warm the climate while stopping oil.

When I look out of the stable after the storm and I see the skies clear, I know that I can walk out and that I will not be pounded by hail. It just happens to repeat each time. You will not convince me that it will continue to hail just because a model says so. A model that cannot predict the present, is not suitable to forecast the future. We should just toss it out along with the pronouns and the Hamas badges. The way forward here is to enshrine into law that no risk can be reported that does not align with actual observations.

Five Mile Ranch eventually got a loan from a local financial institution, who still understand that farms and ranches are a necessary component of the food supply chain and that grazing animals are an essential component to keeping the soil healthy. They interpreted the climate rules accordingly.

A few weeks later, the seasons changed. We had our first cold snap and it was a serious one. Record low temperatures for November and guess what, the newspaper reported the following: “Climate activists on their way back from an anti-Israel protest at McGrath froze to death. Their electric vehicles got stuck in a snowdrift and the battery ran out.”

Instant karma, I’d say.

(If you don’t know McGrath University, check this out, and consider to subscribe!)

(To the interested reader: I have recently been posting short comments and preview snippets on X. A warm welcome to every reader who joins the herd there!)

Excellent discussion. Swiss Re recently noted that property loss costs are growing 5-7% a year. The cited rising construction costs and increased exposure in catastrophe prone areas as the main drivers. In the USA, there has been a net migration toward Florida and Texas, where over 1/2 of all natural catastrophe losses occur …

We keep hearing the same message over and over: "don't try to think for yourself, you don't have the skills", "don't listen to fringe experts", "trust The Science (meaning government alphabet soup)". Because the data is so clearly pointing in another direction than the narrative they are pushing, you have to convince people they are stupid and/or blind to ignore it. They're doing it with covid, they're doing it with gender theory, and they're doing it with climate. Follow the money: our home insurance just increased the wind and hail deductible by 300%. Why? Continental US regions has had large hail and wind long before people settled here, nothing has changed.